How Transformer Shortages and System Dynamics Threaten America’s AI Ambitions

The compounding effects of upstream delays

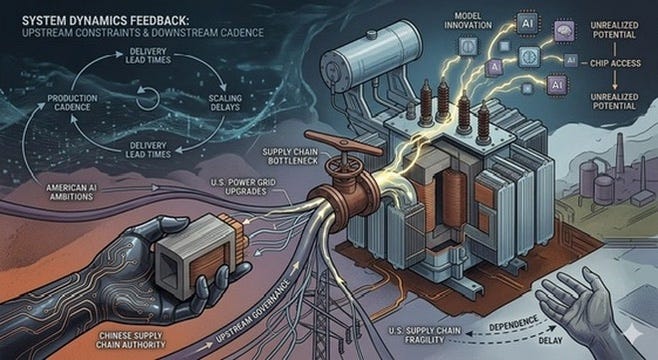

Preface: I have discussed various aspects of the U.S.’ AI sector in recent times. This essay homes in on one aspect of the system — that concerning transformers for the electricity supply network upgrades — which have the potential to generate compounding effects that can set American AI ambitions back substantially. As I have discussed on previous occasions, AI is in effect embodied electricity, and no matter how advanced the AI models themselves are, or that the U.S. has access to the best chips in the world, unless the electricity system can scale in a timely fashion, none of this will ultimately count. While Chinese transformer manufacturers only hold around 50% global market share and, therefore don’t dominate in ways that Chinese supply chains dominate sectors like rare earths, this footprint nonetheless confers upon Chinese firms a not insubstantial amount of supply chain cadence authority. Jay Forrester’s system dynamics lens helps us unpack how upstream governance dictates downstream cadence.

In 2025, China’s transformer exports reached a record 64.6 billion yuan (approximately $9.29 billion), surging nearly 36% year-over-year. Average export prices rose about one-third to roughly 205,000 yuan per unit. Many manufacturers report order books filled through 2027, particularly for data centre applications.

While headlines often focus on rare earths or semiconductors, mundane power transformers illustrate a deeper structural reality in global supply chains. These unremarkable devices — essential for stepping voltage up or down in grids and facilities — have become a critical bottleneck. Their constraints reveal how small frictions, amplified through complex systems, can derail ambitious technological and industrial goals. Jay Forrester’s insights from Industrial Dynamics (1961) explain why these effects matter so profoundly.

The Transformer Crunch in Context

Global electricity demand is rising rapidly due to AI-driven data centres, electrification, renewables integration and grid modernisation. In the United States, data centre power consumption has grown sharply and is projected to reach significantly higher shares of total electricity use in coming years. Aggregate needs for additional firm capacity have been estimated to be in the order of 100 GW over the next few years. Large power transformer lead times now average 128 weeks (over two years), with generator step-up (GSU) units stretching to 144 weeks or even 3–5 years in extreme cases. Distribution transformer waits have extended from pre-pandemic norms of 8–12 weeks to 30–50 weeks or more.

China dominates production, holding roughly 50–60% of global transformer manufacturing capacity. It also leads in key inputs like grain-oriented electrical steel (GOES), which forms the efficient cores of transformers. China accounts for over half of global GOES output, with strong vertical integration from raw processing to finished equipment. This scale enables faster delivery and competitive pricing compared to more fragmented Western capacity.

U.S. imports of transformers and components remain substantial, even as domestic production expansions (e.g., investments by Hitachi, Siemens, GE Vernova, and others totalling nearly $2 billion in North America) are underway. New capacity, however, takes years to permit, build, qualify and ramp. Upstream constraints on materials like GOES — where U.S. domestic production is limited — compound the issue. The result is a seller’s market where Chinese suppliers hold significant scheduling power.

Forrester’s Lens: How Small Delays Become Systemic Crises

Jay Forrester’s system dynamics framework models industrial systems as interconnected stocks, flows, delays and feedback loops. His famous “bullwhip effect” shows how modest variations in downstream demand amplify dramatically upstream. Information distortions, ordering policies, and lead-time delays turn small signals into large oscillations in inventory, production, and pricing.

Applying this to transformers, we can see that delays function as system stabilisers. Inherent manufacturing and qualification times for large power transformers already span years. Administrative “paperwork” frictions — heightened inspections, certification reviews, licensing pauses, or customs holds — add weeks or months without formal bans. These are low-visibility and deniable. We then see how these delays are amplified through loops. A one-month delay on a critical shipment prompts utilities and data centre developers to over-order or seek alternatives frantically. This creates phantom demand spikes. Suppliers see inflated signals and adjust pricing or allocation. Competing projects bid against each other for limited slots, further extending queues.

These effects are reinforced through feedback that then create path dependency effects. Once timelines slip, recovery is nonlinear. A delayed substation idles downstream investments worth billions. Renewables integration slows, power prices rise and financing costs increase. Parallel AI projects compete for the same constrained pool of skilled labour, testing facilities and grid interconnection slots. Early delays lock in longer-term disadvantages.

Forrester’s simulations repeatedly demonstrated counterintuitive outcomes. Policies that ignore systemic structure often worsen problems. In today’s tight-coupled systems, repeated small frictions erode timelines for AI buildout, EV infrastructure and grid resilience far more effectively than isolated shocks. A fortnight here and a month there compound into quarters or years of slippage. In a context in which the U.S. is at least 100 GW of firm capacity short, these compounding effects can play havoc with AI scaling ambitions.

Scale and Upstream Nodes: The Determinative Advantage

China’s position stems from unmatched scale and control over upstream nodes. Transformer production depends on specialised GOES for low-loss cores, high-purity copper windings, insulators, tap changers and integrated assembly. Alternatives in Europe, Japan, South Korea, or the U.S. exist but operate at smaller scale, higher cost, and with their own constraints. Many non-Chinese producers still rely on Chinese inputs for components or raw materials.

This creates “congestion dominance.” In a seller’s market, the economic agent controlling capacity nodes decides allocation, lead times and priorities. Passive-aggressive measures — administrative delays rather than outright bans — exploit system sensitivity without crossing into overt economic warfare. The Global South benefits in this environment, gaining reliable, affordable access for its own electrification and infrastructure needs, while Western markets face premium pricing and queues.

Limited global alternatives amplify the effect. Building new GOES or transformer capacity requires massive capital, technical expertise, permitting and time; often 3–5+ years. Decades of underinvestment in heavy manufacturing in the West left thin buffers. Explosive new demand from AI has exposed the lag.

Raw Material Chokepoints: Copper and the Sulphur Connection

Even China’s advantages face limits. Copper is critical for windings and conductors. Global copper supply, in turn, depends heavily on sulphuric acid for leaching oxide ores. Sulphuric acid derives largely from sulphur, a byproduct of oil and gas processing.

Disruptions in the Strait of Hormuz — through which a large portion of global seaborne sulphur trade flows — have tightened this upstream link. Closures or blockages drive up prices and constrain acid availability. This ripples into copper smelting and refining worldwide, raising costs and potentially slowing mine output and processing. The chain is clear: Hormuz tensions → sulphur/acid constraints → copper tightness → higher costs and delays for transformer windings → further pressure on overall equipment availability. These effects interact with transformer-specific bottlenecks. A system already sensitive to delays becomes even more fragile when multiple layers face simultaneous stress.

How Transformer Bottlenecks Compound U.S. Electricity Supply Network Augmentation

The real-world impacts of these shortages are visible across U.S. electricity networks, where transformer constraints create cascading delays that slow grid modernisation, renewable integration and new load accommodation far beyond isolated project setbacks.

Nearly half (or more than half in some estimates) of U.S. data centres planned for 2026 face delays or cancellations — not due to lack of money capital (with hyperscalers committing over $650 billion in AI-related spending) but because of shortages in transformers, switchgear, related electrical equipment and availability of skilled labour. A single missing high-voltage transformer can hold up a multi-billion-dollar campus for a year or more. AI deployment cycles often target under 18 months, but transformer lead times of 2–5 years clash dramatically with that pace. Developers in regions like Silicon Valley have completed facilities only to leave them idle while awaiting grid connection equipment.

We then have delays to grid interconnection and transmission upgrades. The U.S. interconnection queue holds over 2,000–2,600 GW of proposed generation and storage — roughly double current installed capacity — with average wait times approaching five years. Transformer shortages exacerbate this with new substations and transmission lines requiring large power transformers and GSUs that utilities cannot procure quickly. Projects that clear studies still face multi-year equipment waits, leading to high attrition rates. In PJM and other RTOs, delayed network upgrades triggered by transformer scarcity inflate interconnection costs, sometimes making projects uneconomic.

Renewables developers report projects postponed 1–2 years or more due to transformer unavailability. Aging infrastructure replacement adds pressure as over half of U.S. distribution transformers are 33+ years old and nearing end-of-life. Extreme weather events, such as hurricanes knocking out hundreds of units, force utilities into desperate scrambles in an already undersupplied market. EV charging networks, heat pump adoption and industrial reshoring compete for the same limited pool, creating allocation battles that prioritise certain loads while stalling others.

Add to this the compounding effects in certain regions. In constrained grids (e.g., PJM, ERCOT or California), a delayed 500 kV substation transformer can bottleneck entire clusters of data centres or renewable farms. Costs have risen sharply — prices up 77% or more since 2019, with some reports of 4–6x increases for certain units — raising electricity rates and project financing hurdles. Utilities resort to costly workarounds like temporary diesel generators or curtailment, which undermine reliability goals. Forrester-style amplification is evident as one delay signals scarcity, prompting others to hoard or accelerate orders, further congesting factories and logistics.

These bottlenecks do not act in isolation. A transformer delay at the substation level ripples upstream to generation interconnection and downstream to end-user energisation, multiplying opportunity costs across the network. The asymmetry is stark. Software and chips scale in months, but heavy electrical infrastructure operates on multi-year physical cycles.

Strategic Implications

Transformers exemplify a broader pattern: great-power competition increasingly plays out in the “grey zone” of mature industrial supply chains. Scale, vertical integration and control over key nodes confer quiet leverage. Flashy critical minerals matter, but so do “boring” enablers like electrical steel and copper windings.

Mitigation demands structural thinking. It would involve accelerating domestic and allied capacity for GOES, transformers and related gear. To shorten qualification times, design standardisation would also be required, no tall order. Supply chain orchestration to smooth demand and deliver better supply chain visibility would be needed to buttress the establishment of reserves for long-lead items. All of this is easier said than done. And last but not least, innovation is needed in grid efficiency to stretch existing assets.

Relying on tariffs or reactive policies risks backfiring by distorting signals further. Rebuilding resilient production ecosystems for heavy electrical equipment is a multi-year endeavour. As I have discussed previously, the challenge is that all of this is pitted against a rapidly moving target. In Forrester’s world, system structure produces behaviour. The current transformer congestion — exacerbated by upstream raw material vulnerabilities — warns that America’s AI ambitions rest on fragile foundations. Without addressing these chokepoints, small frictions today will dictate constrained outcomes tomorrow. The window for meaningful correction is narrowing as demand accelerates through 2027 and beyond. Uncorrected, the overall cost disadvantage that U.S. AI systems already face will only compound. Meanwhile, strong usage doesn’t translate into immediate revenues, placing further pressure on cash flow and market valuations.

Thankyou Dr Powell for your insights. You rightly note that despite the current rare earth issues, that “boring” enablers like steel and copper windings are also key. China understands this well, as demonstrated by their emphasis on the circular economy where such materials are recovered, and/or repurposed. Their recent incentivation programs for people to 'trade in', and upgrade a range of consumer durables from which materials like copper are recovered is just one example.

Now add to these supply issues, the possibility of a rogue solar storm and there is absolute chaos. The coming copper shortage isn't going to help. The best option is decentralized supply - more solar panels, etc., rather than massive central distribution upgrades. Some AI datacenters are installing their own natgas powered generation systems. One side issue - wind turbines could be driving an air compressor rather than an electric generator - and, the power is already stored!