China’s Industrial Transition

Beyond the Overcapacity Myth

Preface: In this essay, I return to China’s economic system and ways of understanding its dynamics and evolution, and provide a slightly expanded version of an op-ed recently published. To begin with, I reference the 2025 paper by Suranjana Nabar-Bhaduri and Matías Vernengo in the Review of Political Economy, which provides strong empirical validation of the Kaldor-Verdoorn law in China. Their analysis (1991–2019) shows that output growth powerfully drives productivity growth through demand-led mechanisms, with Verdoorn coefficients near one and GDP shocks dominating productivity outcomes. Recent National Bureau of Statistics data for Q1–April 2026 reinforces this framework in real time: high-tech manufacturing surged 12.6%, high-tech investment and profits led the ongoing structural transformation, PPI turned positive, and modern services consumption accelerated — all amid the transitional overlap of industrial vintages and external shocks from the Iran war.

As China reported 5% GDP growth in Q1 2026, industrial profits of major enterprises surged 15.5% year-on-year, reaching 1.696 trillion yuan. High-tech manufacturing profits soared 47.4%, equipment manufacturing performed strongly, and producer prices (PPI) turned positive after years of deflationary pressure. Yet the familiar chorus of “overcapacity” echoed once again in Western commentary. This static diagnosis — focused on snapshots of factory utilisation, inventory levels, and export volumes — fundamentally misunderstands the dynamic processes underway in the world’s largest industrial economy.

What appears as overcapacity is in reality the transitional overlap of industrial vintages: older, lower-productivity fixed capital from previous investment waves continues operating, generating intense price competition (known in China as neijuan or involution, which I have discussed in detail previously), while newer green, digital, and high-tech capacities scale up. This interregnum is messy and painful in the short term, but it reflects a purposeful process of demand-led structural transformation that is raising the economy’s long-run productive potential.

The Central Role of Kaldor-Verdoorn Dynamics

At the heart of this transition lies the Kaldor-Verdoorn (K-V) law, one of the most important empirical regularities in heterodox economics. First observed by Dutch economist Petrus Johannes Verdoorn in 1949 and later developed by Nicholas Kaldor, the law establishes a strong positive relationship between output growth and labour productivity growth. Unlike the conventional neoclassical view — in which technical progress is largely exogenous and supply-driven — the K-V perspective sees productivity and innovation as largely endogenous to demand expansion.

In their important 2025 paper published in the Review of Political Economy, Suranjana Nabar-Bhaduri and Matías Vernengo provide robust empirical confirmation of these dynamics in China (and India) over the period 1991–2019. Using two sophisticated approaches — partitioned regression analysis and structural vector autoregression (VAR) — the authors demonstrate that output growth powerfully “pulls” productivity growth. For China, they estimated Verdoorn coefficients between approximately 0.89 and 1.05. In practical terms, this means that for every percentage point increase in GDP growth, labor productivity growth rises by nearly the same amount. GDP/output shocks accounted for over 80–90% of the forecast error variance in productivity, while short-term cyclical effects linked to unemployment (Okun’s law) were small and statistically insignificant.

For non-specialist readers, the mechanism works as follows. Autonomous demand — in China’s case, heavily driven by public and strategic investment in infrastructure, industrialisation, and now green and high-tech sectors — acts as the initial catalyst. This demand induces private investment through the accelerator principle and expectations of sustained market growth (a process formalised in Sraffian supermultiplier models). Firms first respond by raising capacity utilisation rates on existing plant and equipment. When high utilisation is sustained over time, several productivity-enhancing processes are activated:

Increasing returns to scale: Larger production volumes allow more efficient use of resources and specialisation;

Learning-by-doing: Workers and engineers gain experience, discovering incremental improvements in processes;

Embodied technical change: New investment incorporates superior machinery, software, and methods; and

Division of labor and structural transformation: Resources shift from lower- to higher-productivity activities.

Intense competition then accelerates the process by pressuring firms to innovate or exit, driving the progressive replacement of obsolete technologies. The result is cumulative causation: demand expansion begets productivity growth, which supports further demand and investment in a virtuous cycle.

In China today, this dynamic is visible in the data. High-tech manufacturing value-added has grown significantly faster than the overall industrial average of 6.1%. Profits have rebounded strongly in upgrading segments even as traditional sectors face margin pressure. The gradual positive shift in PPI signals that newer, more efficient production modes are gaining pricing power as older vintages are progressively rendered obsolete through retrofitting, upgrading programs, and selective scrapping. Policy initiatives such as large-scale equipment renewal and “new quality productive forces” represent a deliberate effort to manage this obsolescence in an orderly fashion rather than through chaotic market-driven collapse.

This demand-led view stands in sharp contrast to mainstream narratives that treat technical progress as an exogenous force and capacity as a fixed constraint. Static “overcapacity” metrics — simple comparisons of output to some estimated efficient level — ignore these temporal and evolutionary realities. They mistake the symptoms of creative destruction during a technological transition for permanent inefficiency.

Short-Term Geopolitical Headwinds; Structural Upgrading Continues

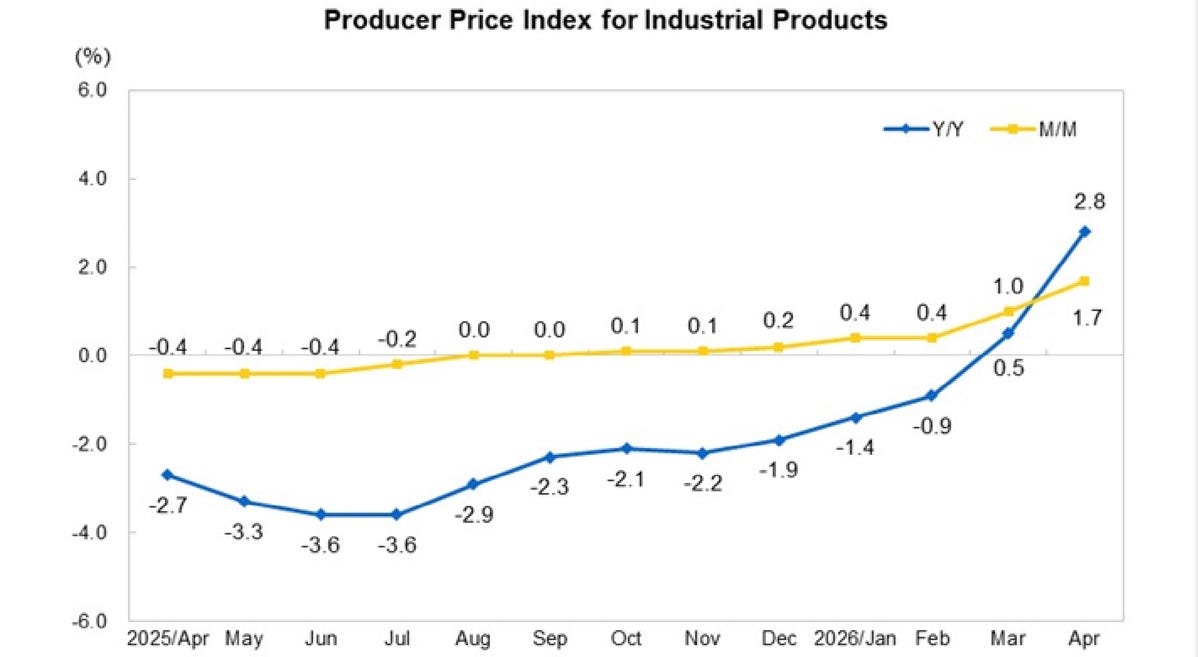

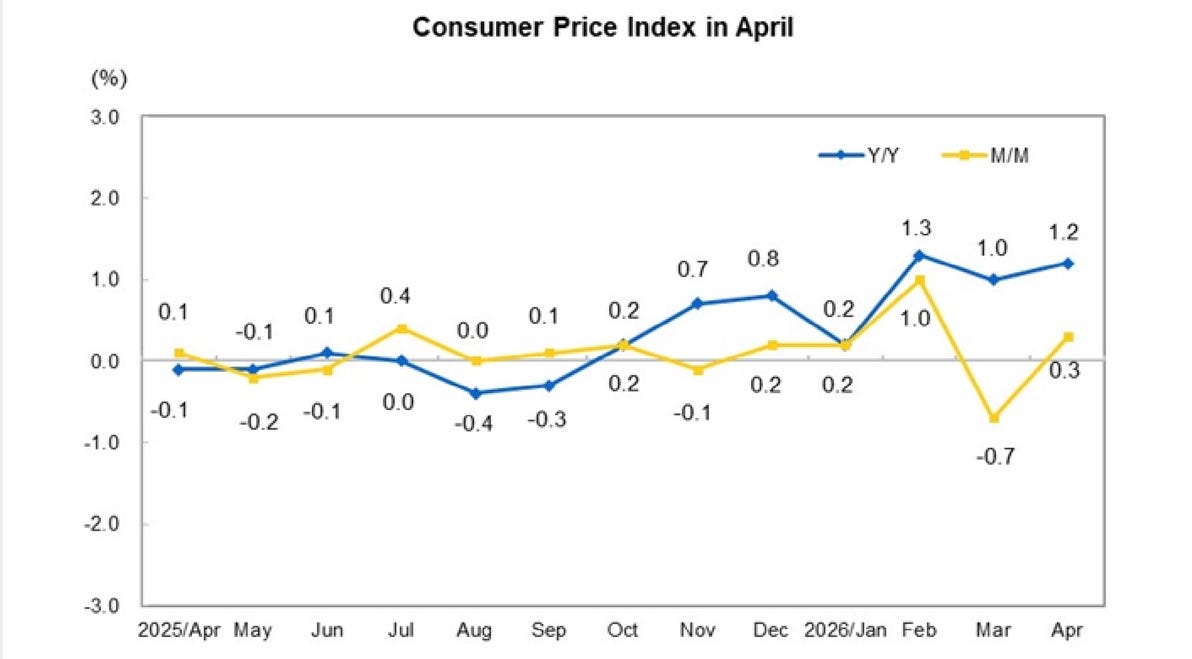

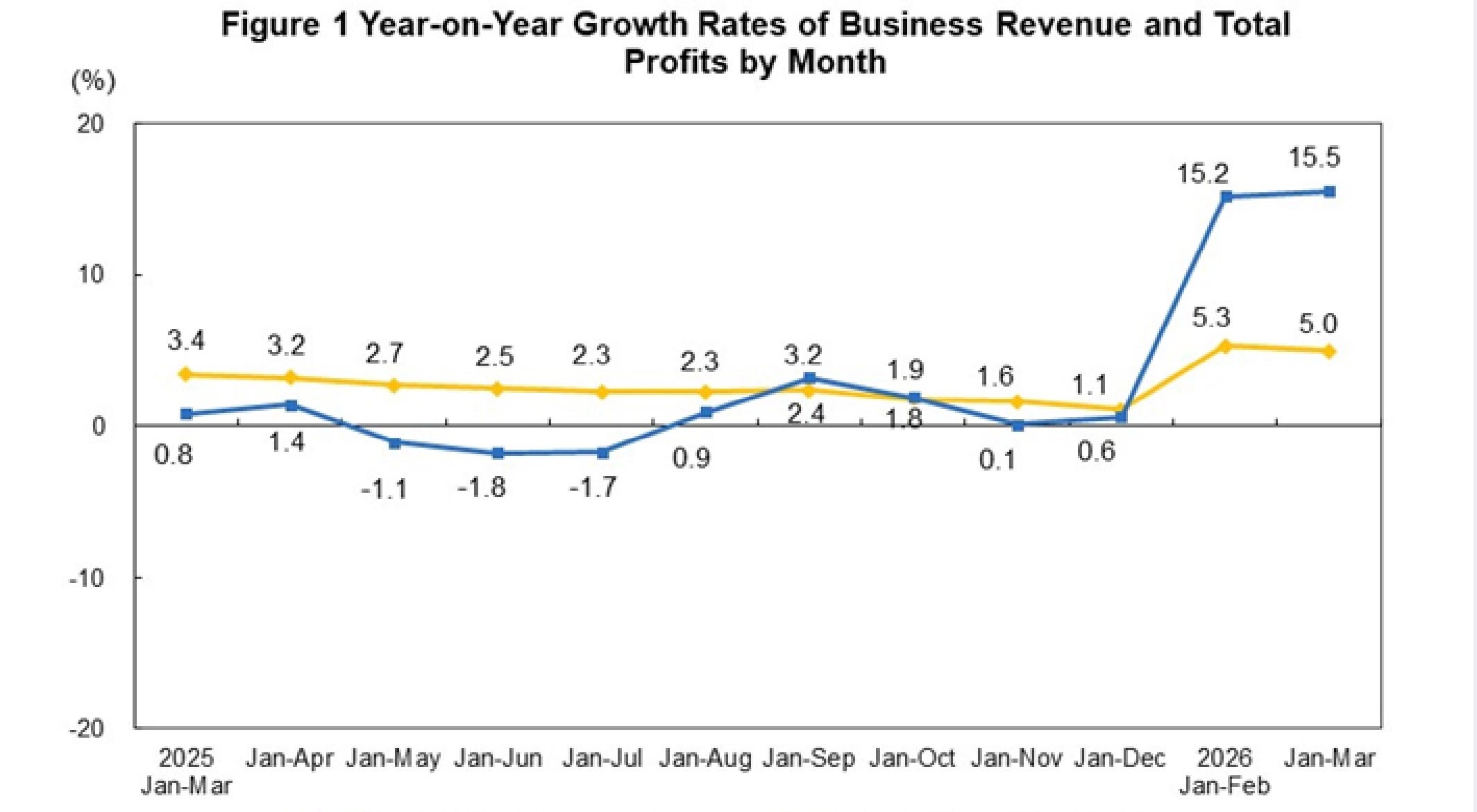

The ongoing war in Iran introduces additional near-term pressures. Disruptions to energy supplies are pushing up input costs (see rising Producer Prices chart below), which may temporarily dampen some investment plans and slow global demand. For China, higher prices (rising CPI, see chart below) could paradoxically encourage a drawdown of household savings to maintain material consumption volumes. Tapered real wage and household income growth — the mirror image of rising profit shares during this capital-deepening phase — reinforces this adjustment (see final chart below showing rising business revenues and profits, which I have also discussed previously). Stronger corporate profits, particularly in upgrading sectors, provide resources for continued reinvestment in new technologies. Well-calibrated policies to support domestic consumption and equipment modernisation can help bridge the transition. (Charts from National Bureau of Statistics of China.)

China’s industrial sector showed solid resilience in the first four months of 2026, per the National Bureau of Statistics release on 18 May, 2026. Industrial value-added for enterprises above designated size grew 5.6% year-on-year. Equipment manufacturing rose 8.7%, while high-tech manufacturing surged 12.6% — that’s 7 percentage points faster than the industrial average. Specific high-tech segments posted impressive gains: production of 3D printing devices (+50.9%), lithium-ion batteries (+36%), and industrial robots (+25.7%). High-tech investment grew 6.1%, with standout increases in aerospace vehicle and equipment (17.9%), computer and office devices (13.9%), and information services (18.1%). Industrial profits in Q1 rose 15.5% to 1.696 trillion yuan, driven by a remarkable 47.4% jump in high-tech manufacturing profits.

These figures highlight ongoing momentum in upgrading sectors even as overall fixed-asset investment declined 1.6% (largely due to ongoing real estate laggardness). Producer prices (PPI) also recovered meaningfully: +0.2% for Jan–April, accelerating to +2.8% in April alone, with purchasing prices up 3.5%. This ends a long deflationary stretch and points to improving pricing power in advanced segments (again, see the chart above).

The ongoing war in Iran has pushed up global energy and commodity costs, raising input prices for energy-intensive industries and creating short-term headwinds for investment and margins. Despite this, high-tech and equipment sectors have largely weathered the storm, supported by sustained demand-pull, policy-backed equipment renewal and productivity gains from upgrading. The resilience underscores that Verdoorn-style dynamics — where output expansion drives learning, scale and embodied technical change — remain active in strategic areas.

Beyond manufacturing, China is experiencing a broader structural shift. The services production index grew 4.9% year-on-year in Jan–April, with modern services leading: information transmission, software and IT services (+10.9%), leasing and business services (+9.3%) and finance (+6.7%). Service retail sales rose 5.6% — significantly faster than overall consumer goods retail (1.9%) — with strong growth in communication information services, tourism/cultural/sports/leisure, and transportation services. Online retail of services increased 8.3%.

This reflects an ongoing reorientation of consumption growth away from traditional tangible goods retail toward a broader, digitally enabled services category (distinct from pure commodity sales). Growth is concentrating in experience-based, information-intensive, and high-value services rather than volume-driven goods. This dual transformation — higher-tech, more energy-efficient production coefficients on the supply side, and a services-oriented consumption shift on the demand side — marks the ongoing unfolding of structural change. It aligns with the move toward “new quality productive forces,” where productivity gains from high-tech manufacturing support rising living standards through diversified services consumption.

Overall, the January–April data paints a picture of an economy that is reasonably successfully navigating transitional frictions and external shocks while advancing its evolutionary path: legacy capacity slowly but surely yields ground to newer, more efficient modes, and consumption patterns evolve in tandem. Sustained policy support for domestic demand and technological transformation will help consolidate these gains.

International Implications and Policy Choices

The international reaction to China’s transition reveals two distinct paths. Advanced economies with mature but increasingly obsolescent industrial sectors, such as those in the EU, have leaned toward heavy protectionism — tariffs, subsidies and investment screening on Chinese EVs, solar panels, batteries, and related goods. This approach is misguided. Many of these economies are simultaneously pursuing remilitarisation while practicing relative fiscal austerity. The combination dampens domestic demand-pull, weakening the very conditions needed for local Kaldor-Verdoorn effects. Rather than blocking Chinese advancements, a more productive strategy would be (selective) openness to Chinese firm investment and technology collaboration. This would accelerate technical propagation, speed the green transition, and allow these economies to capitalise on cost and efficiency gains generated by China’s scale. Chinese firms remain open to expanded investment in the EU, evidenced by the fact that Chinese investment in Europe in 2025 hit a seven year high.

On the other hand, developing economies with limited industrial bases face a different opportunity. Chinese productive capabilities — delivering affordable renewables, machinery, transport equipment, and infrastructure goods — provide powerful tools for their own structural transformation. Recent trade patterns confirm this. Chinese exports have increasingly oriented toward the Global South and Belt and Road partners, now accounting for over half of China’s total trade. While advanced economies remain preoccupied with current account balances and “dumping” concerns, developing nations are harnessing these flows to build industrial foundations.

Moving Beyond Static Tropes

The “overcapacity” debate ultimately reflects a deeper methodological divide. Neoclassical frameworks favour equilibrium analysis and exogenous supply factors. Alternative approaches, grounded in the Kaldor-Verdoorn tradition, emphasise cumulative causation, demand-led growth and evolutionary technical change. China’s experience since the 1990s — and the strong econometric results in the Nabar-Bhaduri and Vernengo study — provide compelling evidence for the latter.

As older industrial modes gradually yield to newer ones, the current period of involution will ease. Q1 2026 indicators — accelerating profits in advanced manufacturing, recovering producer prices and resilient high-tech momentum despite external shocks — suggest the transition is advancing. Understanding this process as demand-induced, competition-driven obsolescence rather than simple excess capacity offers a far more accurate guide for policymakers.

For China, the priority remains sustaining autonomous demand while managing orderly upgrading. For the world, the wiser course is complementary industrial policies that harness rather than resist the global productivity wave. Development is not a zero-sum optimisation problem but an evolutionary process of structural transformation. Static snapshots obscure more than they reveal. Dynamic analysis points toward higher systemic efficiency and shared potential gains — if the politics can catch up with the economics.

Excellent analysis !

I fully agree with Prof. Powell’s judgment: China’s current “involution” and price competition should not be mistaken for permanent, inefficient overcapacity. What we are seeing is the overlap of different industrial vintages. Older capacity from the previous investment cycle is still operating, while new green, high-tech, and digital capacity is expanding. The short-term result is price pressure, profit divergence, and intensified competition.

This is also consistent with my earlier argument that China’s deflationary cycle is largely coming to an end. The key point is that beneath the aggregate numbers, a structural replacement of growth momentum is already underway. New productive forces are replacing old drivers and beginning to pull the economy out of deep deflation.

If developed economies use tariffs, subsidies, and investment screening to block the diffusion of Chinese technologies, they may end up weakening their own green transition and industrial renewal. Developing countries, by contrast, may gain a new industrialization opportunity through China’s low-cost equipment, infrastructure, and renewable-energy products.

This is the piece I've wanted someone with the formal apparatus to write. The move that matters is the one most commentary can't make: treating "overcapacity" not as a snapshot but as the transitional overlap of industrial vintages — old low-productivity capital still running and generating neijuan, while the new green and high-tech vintages scale. That's not a defense of China. It's a different clock.

And the Kaldor-Verdoorn confirmation does real work. Verdoorn coefficients near one, output shocks accounting for 80–90% of productivity variance — this is the econometric spine under what I've been calling the E in R.I.C.E.: evolution as endogenous to demand and competition, not exogenous and supply-given. You've given that mechanism its proper academic bloodline. I'll be citing Nabar-Bhaduri and Vernengo from now on.

Where I'd extend you — not correct you — is one system out.

K-V is a closed loop inside one economy: demand pulls productivity, productivity supports demand, the cycle compounds. It explains, rigorously, why China's engine turns. What it doesn't ask — because it isn't built to — is where the exhaust goes. The same neijuan you read as transitional pain inside China is, on the other side of the Pacific, a permanent deflationary input. One involution, two readings: easing for the system producing it, accumulating for the system absorbing it. I argued this in The Great Divergence — Western structural inflation and Eastern deflationary overcapacity aren't two stories. They're one feedback loop seen from two ends.

That's why the EU response you call self-defeating is worse than self-defeating. You're right that austerity-plus-remilitarisation kills their own K-V conditions. But the deeper bind is that they can't simply open up either, because openness means importing the deflation on China's terms. Tariff and they suffocate their own demand-pull. Open and they import disinflation they can't price. That's not a policy error to be corrected by better economics. It's a structural trap — what I call Hostile Symbiosis: the two industrial systems are physically necessary to each other and physically threatening to each other, at the same time, with no exit that isn't also a death reflex.

So I'd put it this way: you've drawn the engine, and drawn it better than anyone. The piece I'd add is the exhaust pipe — and whose lungs it's connected to. K-V tells us why System B accelerates. It can't tell us why acceleration is, for the other side, indistinguishable from being slowly poisoned. That part isn't economics. It's physics and geography. And it's the half the overcapacity debate will never reach, because it's looking for an equilibrium in a system that doesn't have one.